Snap Inc. Navigates Complex Q1 2026 Landscape with User Growth Masking Core Market Declines and Regulatory Headwinds

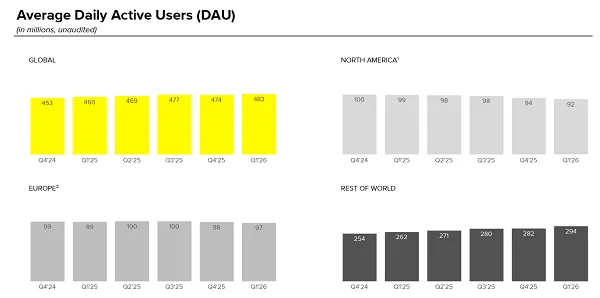

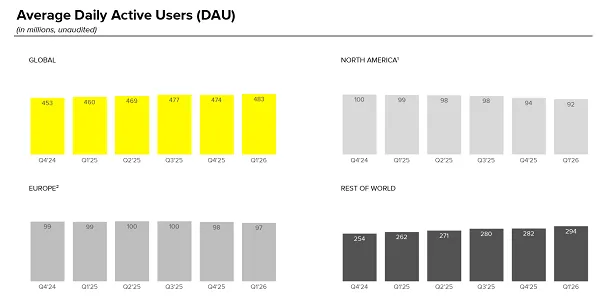

Snap Inc., the parent company behind the popular social media platform Snapchat, has released its Q1 2026 earnings report, painting a nuanced picture of the company’s trajectory. While the report indicates a significant reversal in overall daily active user (DAU) declines observed in the previous quarter and a steady performance in its advertising business, it simultaneously highlights persistent challenges within its most lucrative markets and looming regulatory threats that could disproportionately impact its core demographic. The quarter saw Snap Inc. reach 483 million total daily active users, an increase of 9 million from Q4 2025, halting a prior quarter-over-quarter loss of 3 million users. This topline growth, however, belies a concerning trend of declining engagement in critical North American and European markets, where the majority of the platform’s revenue is generated.

Detailed User Metrics: Global Growth vs. Core Market Contraction

The reported 483 million DAU marks a notable rebound from the previous quarter’s dip, signifying a renewed ability to attract and retain users on a global scale. This growth contributed to an increase in monthly active users (MAU) as well, reaching 956 million, up from 946 million in Q4 2025. While positive on the surface, a deeper dive into the geographic distribution of this growth reveals a strategic conundrum for Snap. The entirety of the 9 million DAU increase originated from "Rest of World" (ROW) regions, where Snap’s business tools are still in nascent stages of development and yield significantly lower average revenue per user (ARPU) compared to established markets.

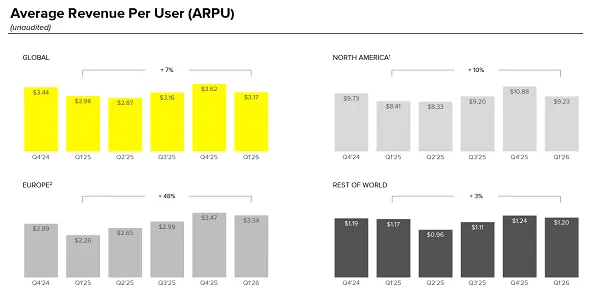

Conversely, Snap’s critical North American market, which remains the primary engine of its profitability, experienced a decline of 2 million daily active users, bringing its total down to 92 million. Similarly, the European Union (EU) saw its DAU shrink by 1 million users quarter-over-quarter. This sustained contraction in high-value markets underscores a fundamental challenge for Snap: while it can grow its user base in emerging economies, monetizing these users at a rate comparable to North America and Europe remains a significant hurdle. For context, in Q4 2025, Snap reported an ARPU of $8.59 in North America, $2.75 in Europe, and a mere $1.18 in the Rest of World. While the Q1 2026 report indicates improvements in ARPU across all regions, the stark disparity persists, meaning that growth in ROW regions contributes disproportionately less to the company’s bottom line. Analysts note that this dynamic places increased pressure on Snap to rapidly develop and scale its advertising infrastructure and business offerings in these growing markets to translate user volume into substantial revenue.

Revenue Performance: Advertising’s Steady Hand

Despite the mixed user engagement figures, Snap’s advertising business demonstrated resilience, reporting $1.53 billion in revenue for Q1 2026. This figure represents a robust 12% year-over-year increase, signaling that Snap’s efforts to diversify its ad offerings and improve advertiser performance are yielding positive results. The company specifically highlighted strong gains driven by Sponsored Snaps, its native advertising format, which integrates promotional content directly into user-generated stories. Furthermore, Dynamic Product Ads, which allow advertisers to automatically showcase product catalogs to relevant users, experienced impressive growth of over 30% year-over-year, with particular strength observed among small and medium-sized business (SMB) customers.

This diversification away from reliance on a few large advertisers and toward broader adoption by SMBs is a strategic positive for Snap. It suggests a more resilient ad platform less susceptible to the spending fluctuations of individual major brands. However, the delicate balance between ad load and user experience remains a critical consideration. As Snap continues to explore new monetization avenues, such as ads within user direct messages (DMs), the potential for user fatigue and complaints about an overwhelming influx of advertising could emerge, potentially eroding the platform’s unique appeal and "connective experience." Maintaining this balance will be paramount to sustaining ad revenue growth without alienating its core user base.

The Regulatory Shadow: Age Restrictions and Their Potent Impact

A significant and growing headwind for Snap Inc., particularly given its strong appeal to younger demographics, is the accelerating global trend towards increased age restrictions on social media use. Following Australia’s pioneering move to implement bans for users under the age of 16, numerous other regions are exploring similar legislative measures. These initiatives are primarily driven by mounting concerns over the negative impacts of social media on adolescent mental health, data privacy, and exposure to inappropriate content.

In February 2026, Snapchat itself reported the tangible consequences of Australia’s teen ban, confirming that it had been compelled to lock or disable approximately 415,000 user accounts within the country. Given Australia’s population of around 27 million, this figure underscores the significant potential impact such bans could have if adopted by larger nations. The report specifically cited Germany (population 84 million), the United Kingdom (69 million), and Spain (49 million) as countries actively considering similar social media bans for minors. Should these populous European nations enact comparable legislation, the cumulative effect on Snap’s user base and broader growth plans could be profound, potentially resulting in millions of account restrictions.

The disproportionate impact on Snapchat stems from its established popularity among younger audiences, often serving as a primary communication tool for teens. While other platforms also cater to younger users, Snapchat’s ephemeral content and direct messaging focus have historically resonated strongly with this demographic. The operational challenges associated with robust age verification, coupled with the potential loss of a substantial segment of its user base, represent a major risk factor that could severely constrain Snap’s future growth and market capitalization. The company faces the dual challenge of adapting to a stricter regulatory environment while simultaneously innovating to retain and attract users within permissible age brackets, potentially requiring a re-evaluation of its product development and marketing strategies.

Financial Health and Operational Efficiency

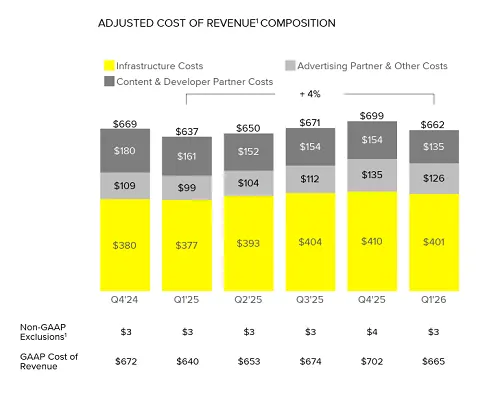

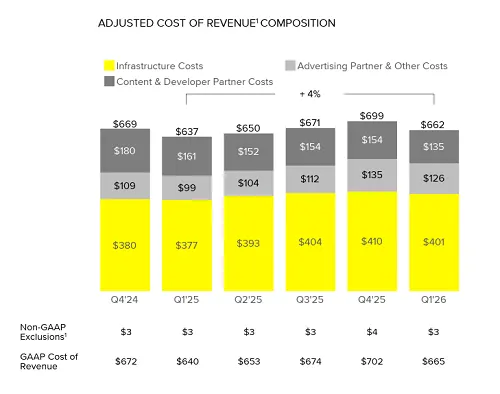

Despite the year-over-year revenue increase, the Q1 2026 earnings report indicates that Snap continues to grapple with high operational costs. The cost of revenue, research and development (R&D), sales and marketing, and general and administrative expenses collectively represent a substantial portion of the company’s expenditure. While specific net profit/loss figures were not detailed in the provided content, the emphasis on high costs suggests ongoing pressures on profitability.

In response to these financial realities, Snap Inc. has been actively pursuing cost-cutting measures. A notable initiative in the recent past was the layoff of 16% of its full-time staff, an action taken to improve overall viability and streamline operations. These restructuring efforts aim to enhance efficiency and ensure a leaner organizational structure as the company continues to mature its advertising business and explore new growth opportunities. However, the persistent challenge of balancing innovation and growth investments with cost control remains central to Snap’s financial strategy. Investors will be closely scrutinizing future reports for signs of sustained profitability and improved operating margins, especially as the company navigates a competitive and increasingly regulated landscape.

Strategic Imperatives: Navigating the "Crucible Moment"

Snap CEO Evan Spiegel has characterized this period as a "crucible moment" for the company, a term that conveys a time of severe trial or a point at which forces interact to produce something new. This candid assessment reflects the multi-faceted challenges Snap faces: competing fiercely with tech giants like Meta and Google, fending off agile startups vying for its core market, and adapting to evolving user behaviors and regulatory demands.

Snap’s stated growth strategy, as presented to investors, hinges on several key pillars:

- Grow and engage our community: As noted, this objective presents a dichotomy, with global expansion offset by contraction in core profitable markets. The long-term viability of this pillar depends on converting ROW users into higher-value advertising segments.

- Innovate and differentiate our products: The report acknowledges that Snapchat’s innovation has not "evolved a lot in recent years," with the most prominent recent addition, Spotlight, being a direct response to TikTok’s success. While effective, this reactive approach raises questions about Snap’s capacity for groundbreaking originality, which was once a hallmark of the platform. The growth of Snapchat+ subscription revenue is positive, indicating a willingness of users to pay for premium features, but it is unlikely to ever match the scale of ad revenue.

- Improve advertiser performance: This is directly tied to ARPU growth and the expansion of ad formats and targeting capabilities. The success of Sponsored Snaps and Dynamic Product Ads demonstrates progress, but the potential for user backlash from increased ad density remains a risk.

- Build a future with AR: This represents Snap’s boldest long-term bet, envisioning a future where augmented reality is seamlessly integrated into daily life.

Innovation and the Future of AR

Snap’s commitment to augmented reality (AR) remains a cornerstone of its long-term vision, manifested primarily through its Spectacles line of AR glasses. The company is reportedly still aiming for a launch of its latest AR device this year. However, the path to mainstream AR adoption is fraught with challenges, and Snap faces stiff competition. Reports suggest that Snap’s current AR device, described as "chunky" and "heavy," may already be technologically inferior to competing offerings, such as Meta’s anticipated AI glasses.

Meta, a formidable competitor with vast resources, has outlined plans to launch its own advanced AR glasses around 2027, building on its experience with Ray-Ban Stories and extensive R&D in the metaverse. Apple is also a major player in the mixed reality space with its Vision Pro. The competitive landscape for AR wearables is rapidly intensifying, and consumer demand for such devices, especially at premium price points, is still largely unproven. Snap’s ability to carve out a meaningful market share and drive significant revenue from its AR ventures is highly speculative, particularly given the historical challenges and limited commercial success of previous Spectacles iterations. The investment required for cutting-edge AR development is substantial, adding another layer of financial pressure on a company already managing high costs and navigating complex market dynamics.

Analyst Outlook and Long-Term Viability

The Q1 2026 earnings report presents a mixed bag for investors. While the return to overall user growth and steady ad revenue growth offer some relief, the underlying trends of declining engagement in core profitable markets and the looming threat of widespread age restrictions cast a long shadow over Snap’s future. Analysts are likely to maintain a cautious stance, emphasizing the need for Snap to demonstrate a clear and sustainable path to profitability, particularly by improving ARPU in its rapidly expanding ROW markets.

The "crucible moment" articulated by CEO Evan Spiegel aptly summarizes the critical juncture Snap finds itself in. The company must not only innovate effectively and differentiate its products in a crowded social media landscape but also strategically navigate regulatory headwinds and translate its global user base into tangible financial returns. The long-term viability of Snap Inc. will hinge on its ability to evolve beyond its current limitations, broaden its appeal beyond a transient younger demographic, and successfully execute on its ambitious AR vision amidst formidable competition. The coming quarters will be pivotal in determining whether Snap can emerge from this trial stronger and more competitive, or if its growth will remain inherently confined by these structural and market challenges.

{kind=link}