The Evolution of E-commerce Returns in Europe Navigating Logistical Challenges Financial Pressures and Sustainability Demands

The modern e-commerce landscape in Europe has undergone a fundamental shift, where the completion of a transaction no longer signals the end of the customer journey but rather the midpoint of a potential circular process. Returns have transitioned from being a peripheral logistical concern to a central pillar of retail strategy, influencing everything from profit margins to brand loyalty. As digital penetration deepens across the continent, the volume of returned merchandise has reached unprecedented levels, forcing merchants to rethink the "free return" models that once defined the industry’s growth phase. This comprehensive analysis explores the current state of European e-commerce returns, the systemic challenges facing retailers, and the strategic shifts necessary to maintain viability in an increasingly complex market.

The Statistical Landscape of European Returns

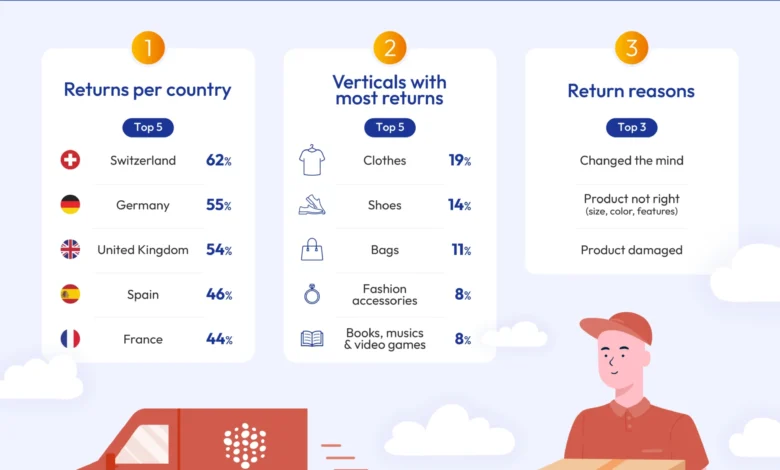

In the current European market, return rates have stabilized at a high plateau, typically ranging between 30% and 40% for general online purchases. However, these figures mask significant geographical disparities that reflect deep-seated cultural shopping habits and varying levels of consumer protection maturity. According to recent 2023 data from Statista, Switzerland currently leads the continent with the highest return rate, with 62% of online shoppers returning at least one item annually. Germany follows closely at 55%, a figure often attributed to the nation’s long-standing history of mail-order catalog shopping, which established a "try-before-you-buy" culture decades before the rise of the internet. The United Kingdom ranks third at 54%, highlighting a highly competitive market where consumer expectations for flexible return policies are among the highest in the world.

These statistics represent a significant financial burden. Industry analysts estimate that the average cost of processing a single return in Europe—factoring in transport, inspection, and restocking—ranges between €15 and €25. When applied to millions of transactions, the impact on the bottom line is profound. Consequently, the era of universal free returns is beginning to wane. In 2022 and 2023, major retail conglomerates, including Inditex (Zara) and H&M, began introducing nominal fees for mail-in returns in several European markets, marking a pivotal shift in the industry’s approach to reverse logistics.

Sector-Specific Trends and the Rise of Bracketing

The impact of returns is not distributed equally across all retail sectors. The fashion and apparel industry remains the most heavily affected, with some sub-sectors reporting return rates as high as 50% or more. This is driven largely by the subjective nature of fit and style, but also by a growing consumer trend known as "bracketing." Bracketing occurs when a shopper purchases the same item in multiple sizes or colors with the explicit intention of keeping only one and returning the rest. While this behavior mimics the fitting room experience, it creates immense logistical strain and inventory "dead zones" where products are in transit and unavailable for sale to other customers.

Other sectors face different challenges. Electronics and household items, while maintaining lower return rates (approximately 6% each), often involve higher-value goods where the cost of damage during return transit or the loss of resale value due to opened packaging is much more significant. For these merchants, the challenge is not the volume of returns, but the technical complexity of refurbishing and recertifying products for the secondary market.

A Chronology of Return Policy Evolution

To understand the current crisis, one must look at the timeline of how returns became a standard expectation in Europe:

- The 2011 EU Consumer Rights Directive: This landmark legislation established a mandatory 14-day "right of withdrawal" for most online purchases across the European Union. It set the baseline for consumer trust but also institutionalized the return process.

- The "Zalando Effect" (2010s): Companies like Zalando and ASOS used 100-day return windows and free shipping as aggressive customer acquisition tools, training an entire generation of shoppers to view the home as a fitting room.

- The Post-Pandemic Correction (2021–Present): Following the e-commerce surge during COVID-19, rising fuel costs, labor shortages, and inflation made the "free return" model unsustainable. This period has seen the introduction of return fees and the implementation of AI-driven sizing tools to prevent returns at the source.

Logistical and Cross-Border Complexities

Managing returns within a single country is a significant task, but the European market’s cross-border nature adds layers of regulatory and logistical difficulty. Merchants selling from a hub in the Netherlands to customers in Italy or Poland must navigate varying postal systems and consumer expectations.

Cross-border regulations remain a primary hurdle. While the EU provides a unified framework, specific national requirements for labeling, environmental taxes, and waste management (such as the AGEC law in France) require merchants to maintain a highly adaptable logistical infrastructure. Furthermore, customs documentation for returns coming from outside the EU—specifically the United Kingdom post-Brexit—has introduced delays and additional costs that frequently exceed the value of the returned item itself.

Logistical efficiency is further hampered by the "reverse mile." Unlike outbound shipping, which is optimized for speed and volume, inbound returns are often fragmented. Items arrive at different times, in varying conditions, and often without original packaging. Establishing local return hubs has become a popular strategy for international sellers, allowing them to consolidate returns within a country before shipping them back to a central warehouse in bulk, thereby reducing international freight costs.

The Environmental Toll and Sustainability Mandates

Beyond the financial metrics, the ecological impact of e-commerce returns has moved to the forefront of the corporate social responsibility (CSR) agenda. The "hidden footprint" of a returned parcel includes the carbon emissions of a second (and sometimes third) journey, the consumption of single-use packaging materials, and the potential for returned goods to end up in landfills if they cannot be easily resold.

In Europe, where the Green Deal and circular economy initiatives are driving policy, retailers are under increasing pressure to disclose and reduce their return-related emissions. This has led to the rise of "green returns," where customers are encouraged to drop off items at centralized collection points rather than requesting home pickups. Some retailers are also experimenting with "keep-it" subsidies, where for low-value items, the merchant provides a partial refund and allows the customer to keep the product, avoiding the carbon cost of shipping it back.

Strategic Optimization: Data, Technology, and Policy

To survive the "return culture," European e-commerce merchants are adopting a multi-faceted optimization strategy:

1. Data-Driven Prevention: By analyzing return data, merchants can identify "serial returners" or products with consistent sizing issues. If a specific dress is returned 60% of the time for being "too small," the merchant can update the product description with a proactive warning or adjust the sizing chart.

2. Technological Integration: Augmented Reality (AR) "virtual try-on" tools and AI-powered size recommenders are becoming standard. By helping the customer make the right choice the first time, retailers can cut return rates by an estimated 10% to 15%.

3. Policy Transparency: A user-friendly return policy does not necessarily mean a "free" policy. Consumers increasingly value clarity and ease over cost. Providing a pre-printed label or a QR code for a paperless return at a local kiosk can often result in higher customer satisfaction than a free return that requires the customer to find a printer and a specific courier.

4. The Circular Economy and Second-Life Sales: Forward-thinking retailers are integrating "re-commerce" into their platforms. Instead of liquidating returned goods, they are creating "outlet" or "pre-loved" sections on their own websites, capturing value from items that might otherwise be written off.

Broader Implications for the European Retail Market

The management of returns has become a competitive differentiator. In a market where customer acquisition costs are skyrocketing, the ability to handle a return professionally can turn a potentially negative experience into a loyalty-building moment. Conversely, poor return management—characterized by delayed refunds and opaque processes—is one of the fastest ways to lose a customer in the European market.

As we look toward the future, the integration of returns into the broader supply chain strategy will be essential. The industry is moving toward a model of "responsible consumption," where the costs of the circular economy are shared more equitably between the merchant, the consumer, and the logistical provider. For e-commerce sellers in Europe, the goal is no longer just to sell a product, but to manage the entire lifecycle of that product in a way that is profitable, sustainable, and respectful of consumer rights. Those who master this balance will lead the next phase of European digital commerce, while those who ignore the complexities of the return process risk being buried by its costs.

{kind=link}